Traditional IRAs and other qualified retirement funds allow pre-tax contributions that grow tax-deferred, but withdrawals (including conversions) are taxed as ordinary income. Roth IRAs, by contrast, are funded with after-tax dollars, enabling tax-free qualified withdrawals and growth. Roth IRAs are not subject to required minimum distributions (RMDs), and heirs do not pay taxes when inherited.

Converting assets requires recognizing their fair market value (FMV) as taxable income in the year of conversion. For large accounts or those in higher tax brackets, this can trigger significant immediate tax liability – sometimes pushing taxpayers into higher brackets or affecting eligibility for other tax benefits.

The goal of any conversion strategy is to minimize the taxable amount while maximizing future tax-free growth. Publicly traded securities (stocks, bonds, mutual funds) typically have straightforward, market-based valuations, limiting flexibility. Alternative assets, however, open the door to more nuanced approaches — particularly real estate held through private structures.

Self-Directed IRAs permit investments in alternatives such as real estate, private equity, and partnership interests. While Roth conversions are not restricted to accredited investors, the use of private market real estate interests generally requires such by the IRS Code.

The IRS Code allows for a wide range of real estate investment strategies; this article will focus on larger Sponsor funds that provide access to appropriate, diversified investment structures that meet IRS requirements.

How Valuation Discounts Work in Practice: Two Applicable Strategies

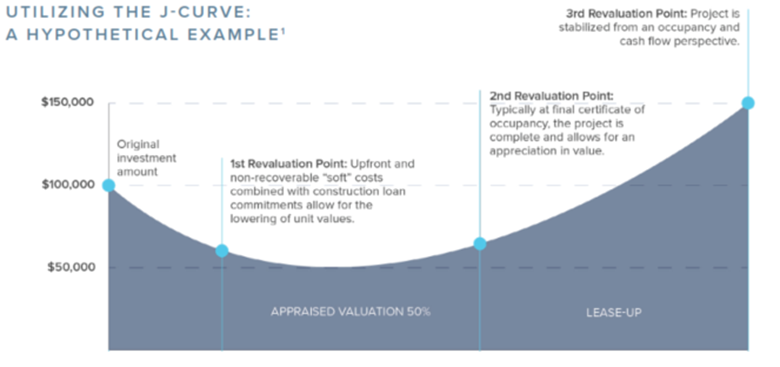

- Natural Valuation Dips via the J-Curve Common to Development Projects.

Real estate development follows a predictable pattern of upfront soft costs, including permits, fees, design, and initial construction, plus execution risk, which temporarily depresses the asset’s value. An investment of $100,000 might be appraised at only $65,000-$70,000 mid-construction, before rebounding upon stabilization and leasing. Converting the IRA during this interim low point means paying taxes on the reduced FMV. Once inside the Roth IRA, the project’s subsequent appreciation and cash flows grow entirely tax-free. - Formal Valuation Discounts: DLOM and DLOC.

Even without a development dip, the ownership interest itself can qualify for discounts:- Discount for Lack of Marketability (DLOM): reflects the difficulty of quickly selling an illiquid private asset (typically 10-40%).

- Discount for Lack of Control (DLOC): Accounts for a minority or non-controlling stake with limited influence over management decisions (typically 10-35%).

Hypothetical Example

Self-Directed IRA (SDIRA) invests $100,000 in an appropriate real estate fund. A qualified independent appraiser determines that, after applying the 30% combined discount, the FMV of the IRA’s interest is $70,000. The conversion taxes only $70,000 instead of the $100,000, saving roughly $10,500 in taxes at a 35% marginal rate. The full asset value later recovers and grows inside the Roth. The tax savings amount increases with investment size.

Implementation Steps and Requirements

- Invest strategically: Use the traditional IRA to fund a suitable private real estate fund. A common source of rollover funds is a prior employer’s 401(k).

- Obtain a qualified appraisal (often recommended or commissioned by the Sponsor): Engage an independent, credentialed appraiser experienced in IRS-compliant valuations for retirement accounts. The report must document methodology, comparable transactions, and discount justifications.

- Time the conversion: Align with the point of lowest defensible FMV (mid-construction or after applying discounts). When justified, span a portion of the conversion, known as “creeping conversion,” over multiple tax reporting periods.

- Custodian reporting: The SDIRA custodian relies on the appraisal to report the discounted FMV on Form 5498 and issues a Form 1099-R reflecting the lower taxable amount for the conversion.

- Pay taxes from non-IRA funds: Using cash preserves more of the account balance inside the Roth, putting more dollars to work building wealth.

Benefits and Tax Optimization Potential

- Once funds are converted to a Roth IRA, all future investment earnings grow tax-free, and qualified withdrawals are also tax-free (after a minimum 5-year hold). This can lead to significantly higher after-tax wealth in retirement, especially if you anticipate being in a higher tax bracket in the future. Also, the resulting lower conversion’s taxable base can potentially keep the taxpayer in a lower bracket.

- Amplified tax-free growth: More assets (and future appreciation) shift to Roth’s tax-free environment.

- Unlike traditional IRAs, Roth IRAs are not subject to RMDs during the account holder’s lifetime. This allows assets to continue to compound tax-free, providing greater control over cash flow, income planning, and tax strategy in retirement.

- Leverage with other tools: Combine with tax-loss harvesting or charitable strategies to further offset the conversion tax.

Risks, Considerations, and IRS Scrutiny

The IRS requires accurate FMV reporting for all retirement plan assets and closely examines large or aggressive valuations during audits. Key risks include:

- Insufficient documentation: Valuations lacking rigorous methodology or independence may be disallowed, triggering additional taxes, penalties, and interest.

- Pre-tax funds converted to a Roth IRA are subject to income tax in the year of conversion. This can create substantial tax liability if not planned carefully.

- Five-year rule: Funds converted to a Roth IRA must remain invested for five years from the conversion, or they may be subject to penalties.

- Market and project risk: The J-curve dip is not guaranteed; development projects carry execution, cost-overrun, and economic risks.

State taxes, phase-outs of other deductions, and Medicare surtaxes should also factor into modeling.

Conclusion: A Tool for Sophisticated Investors

Real estate valuation discounts represent an advanced, IRS-compliant method to mitigate the tax cost of Roth conversions when alternative assets are involved. By combining the temporary valuation dynamics of development projects with established discounts for illiquidity and lack of control — supported by independent appraisals — investors can potentially transfer more wealth into a tax-free environment. However, success hinges on meticulous planning, qualified professionals (tax advisors, appraisers, and SDIRA custodians), and a defensible valuation file.

Disclaimer notice

This strategy is not a universal solution and carries meaningful risks and costs. It is intended for informational purposes only and does not constitute tax, legal, or investment advice. Illustrations used are hypothetical and for information only.1 They do not represent that any account will or is likely to achieve profits or losses like those shown.

Any related offering is only made by a Private Placement Memorandum. Individual circumstances vary widely; always consult qualified professionals before pursuing any Roth conversion or alternative-asset strategy. SREI Group, or its affiliates, cannot provide tax or legal advice.

Sale-Leaseback

Sale-Leaseback